5 Common Credit Report Errors in Minnesota (and How to Fix Them)

5 Common Credit Report Errors in Minnesota (and How to Fix Them)

Category: Credit Education • Reading Time: 8 min read • Author: Carlos Hawkins, Founder of AIM Credit Repair LLC

IMPORTANT DISCLOSURE

AIM Credit Repair LLC is not a law firm and does not provide legal advice. You have the right to dispute inaccurate information on your credit report for free by contacting the credit bureaus directly. You are not required to use a credit repair company or hire anyone to assist you with this process.

For free resources and information about your rights, visit:

- Consumer Financial Protection Bureau: consumerfinance.gov

- Federal Trade Commission: reportfraud.ftc.gov

- Minnesota Attorney General Consumer Protection: ag.state.mn.us

Minnesota Residents: Under the Minnesota Credit Services Organization Act, you have the right to cancel any credit services agreement within 5 business days without penalty. You will not be charged any fees before services are performed.

The Costly Reality of Credit Report Errors in Minnesota

Whether you are preparing to buy a home in Minneapolis, financing a vehicle in St. Paul, or applying for a business loan in Hugo, your credit score is the gatekeeper to your financial goals. Unfortunately, the data used to calculate that score is frequently flawed.

According to a landmark study by the Federal Trade Commission (FTC), one in four Americans has an error on their credit report. Even more concerning, approximately 20% of those errors are serious enough to actively drag down credit scores, resulting in higher interest rates, loan denials, or increased insurance premiums.

At AIM Credit Repair LLC in Hugo, Minnesota, we review hundreds of consumer credit files every month. We consistently see how minor reporting mistakes turn into major financial roadblocks for local families.

Below, we break down the five most common credit report errors we encounter in Minnesota, how to spot them, and the exact steps you need to take to correct them.

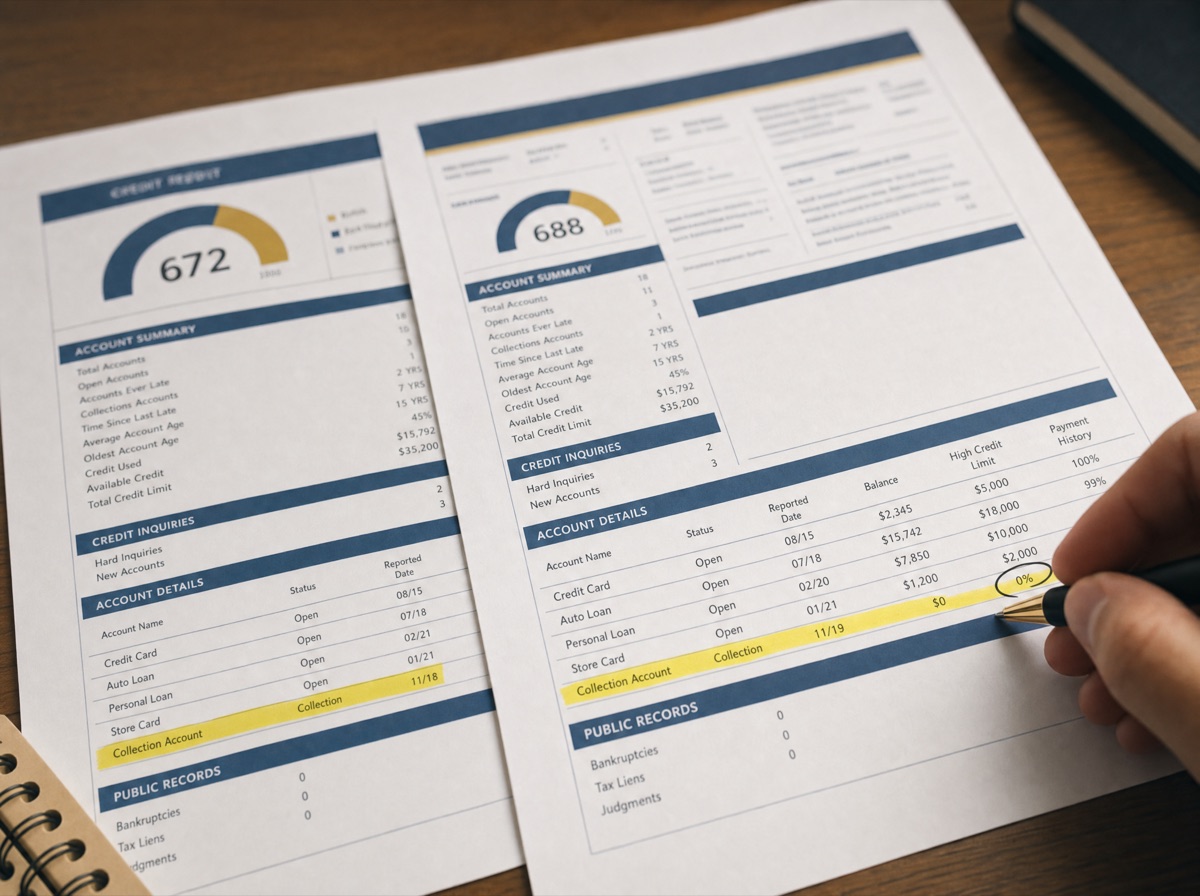

The 5 Most Common Credit Report Errors

1. Identity Errors and "Mixed Files"

Identity errors occur when someone else's financial information is mistakenly merged into your credit profile. This is one of the most damaging errors because it often introduces high balances, late payments, or collection accounts that do not belong to you.

- Why It Happens: Credit bureaus handle massive volumes of data. If another consumer has a similar name, a similar Social Security number (SSN), or lives at a previous address of yours, the bureau's automated systems may accidentally merge your files. This is known in the industry as a "mixed file." It can also be the first warning sign of active identity theft.

- How to Spot It: Carefully review the personal information section of your credit report. Look for unfamiliar addresses, variations of your name, incorrect birthdates, or accounts you have no record of opening.

- What to Do: File an immediate dispute with the credit bureau reporting the error. If identity theft is suspected, place a fraud alert on your credit file and file a report at IdentityTheft.gov.

2. Duplicate Accounts (Double-Reporting)

Duplicate accounts occur when a single debt is listed multiple times on your credit report, making it appear as though you owe twice as much money as you actually do.

- Why It Happens: This frequently occurs when a creditor sells a delinquent account to a debt buyer or transfers it to a collection agency. Instead of updating the original account to show a zero balance and noting that it was transferred, both the original creditor and the collection agency may list the debt as active and unpaid.

- How to Spot It: Look for identical account balances, original loan amounts, payment histories, and opening dates listed under two or more different creditor names.

- What to Do: Dispute the duplicate listing with the credit bureaus. Under the Fair Credit Reporting Act (FCRA), a single debt cannot be reported in a way that artificially inflates your debt-to-limit ratio or total outstanding liabilities.

3. Incorrect Payment Statuses

Your payment history is the single largest factor in your credit score, accounting for 35% of your FICO® Score. A single reported late payment (30, 60, or 90 days past due) can cause an immediate and severe drop in your score.

- Why It Happens: Lenders rely on automated batch-reporting systems. System glitches, processing delays, or simple human error can result in an on-time payment being marked as late.

- How to Spot It: Compare your personal bank statements, canceled checks, or online payment confirmations against the monthly payment grid on your credit report.

- What to Do: Gather your physical proof of payment (such as a bank statement showing the funds leaving your account before the due date). Submit this evidence alongside a formal dispute letter to both the credit bureau and the creditor (the "furnisher" of the data).

4. Outdated "Zombie" Information

Negative credit markers are not meant to follow you forever. Under federal law, most negative information must be removed from your credit report after a specific period.

- Why It Happens: Credit bureaus do not always purge expired data automatically. Sometimes, collection agencies will "re-age" an old debt by changing the "date of first delinquency" to make the debt appear newer than it is, keeping it on your report illegally.

- How to Spot It: Check the dates on negative items such as late payments, repossessions, or charged-off accounts. Under the FCRA:

- Late payments, collections, and charge-offs must be removed after 7 years from the date of the first missed payment.

- Chapter 7 bankruptcies must be removed after 10 years.

- What to Do: If you spot a negative item that is past its legal reporting limit, dispute it immediately on the grounds that it is obsolete.

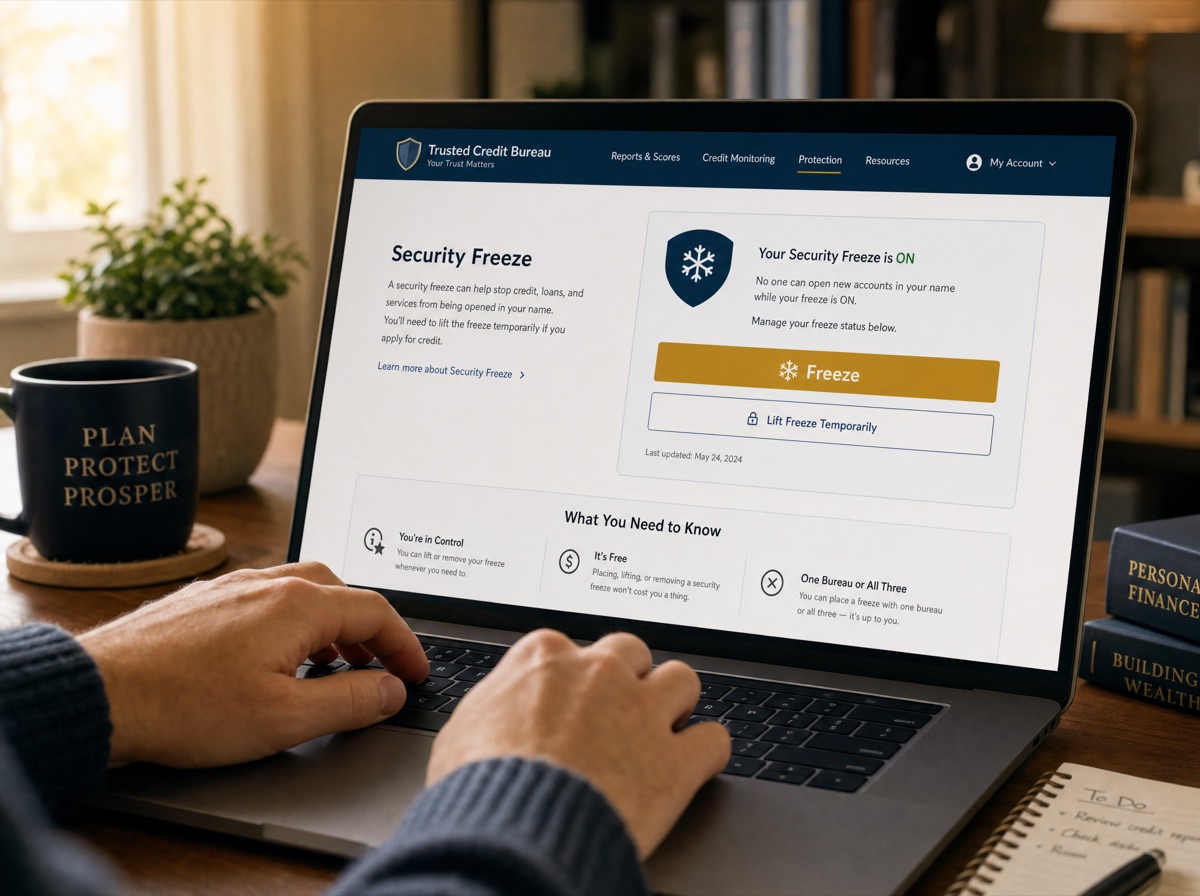

5. Fraudulent Accounts from Active Identity Theft

Unlike a passive data entry error, this occurs when an unauthorized individual actively uses your personal information to open new lines of credit.

-

Why It Happens: Data breaches, phishing scams, or lost physical documents allow identity thieves to acquire your SSN, name, and date of birth to open fraudulent credit cards, personal loans, or mobile phone accounts.

-

How to Spot It: Look for recent hard inquiries that you did not authorize, along with newly opened accounts that you do not recognize.

-

What to Do: This requires a multi-step response:

- Freeze Your Credit: Contact Experian, Equifax, and TransUnion to freeze your credit files. This is free and prevents anyone from opening new accounts in your name.

- File a Federal Report: Submit an identity theft report at IdentityTheft.gov.

- File a Local Police Report: Contact your local Minnesota police department (such as the Hugo or Minneapolis Police) to file an official report.

- Dispute: Send copies of your identity theft report and police report to the credit bureaus to have the fraudulent accounts blocked and permanently removed.

How to Check Your Credit Reports for Free

Under federal law, you are entitled to review your credit reports from the three major national bureaus—Equifax, Experian, and TransUnion—completely free of charge.

- The Official Portal: Visit AnnualCreditReport.com. This is the only official, government-mandated website for securing your free weekly or annual credit reports.

- Why Check All Three? Lenders are not required to report your account history to all three bureaus. A major error might appear on your Experian report but be completely absent from your TransUnion or Equifax reports. To protect your credit, you must review all three files individually.

Step-by-Step: How to Dispute a Credit Report Error

If you identify an inaccuracy on your credit report, you have the legal right to challenge it. Follow this structured process to ensure your dispute is processed effectively:

- Document the Error: Print or take a clear screenshot of the credit report page containing the error. Circle or highlight the specific line item that is incorrect.

- Gather Supporting Evidence: Collect bank statements, payment receipts, correspondence with the lender, or identity theft reports that prove your claim.

- Draft a Formal Dispute Letter: Clearly state your name, address, and SSN. Identify the specific account number and the exact error. Explain clearly why the information is inaccurate and state what action you want taken (e.g., "Please delete this duplicate account" or "Please update the payment status to current"). The Consumer Financial Protection Bureau (CFPB) publishes free, ready-to-use sample dispute letters you can adapt for this step at consumerfinance.gov.

- Send via Certified Mail: Mail your dispute package to the credit bureau. Always send it via Certified Mail with a Return Receipt Requested. This provides you with legal proof of the date the bureau received your dispute.

- Notify the Creditor: Send a duplicate copy of your dispute and evidence to the creditor that reported the information.

- Wait for the Investigation: Under the FCRA, credit bureaus generally have 30 days (sometimes extended to 45 days if you send additional information during the investigation) to investigate and respond to your dispute.

Frequently Asked Questions

How long does a credit dispute take in Minnesota?

Under federal law, credit bureaus must investigate and respond to your dispute within 30 days of receiving your letter. If they cannot verify the accuracy of the disputed item within that timeframe, they are legally required to update or delete it.

Can I dispute credit report errors on my own?

Yes. You have the absolute right to dispute any inaccurate information on your credit report for free directly with the credit bureaus. You do not need to hire a professional service to do this.

What is the Minnesota Credit Services Organization Act?

This is a state consumer protection law (Minnesota Statutes Chapter 332G) that regulates credit repair companies operating in Minnesota. It grants Minnesota residents the right to cancel any credit services agreement within 5 business days without penalty and prohibits companies from charging upfront fees before services are fully performed.

Professional Credit Coaching and Dispute Assistance

While you can manage the dispute process independently, many Minnesota residents find the paperwork, tracking, and constant follow-ups with creditors and bureaus to be overwhelming.

At AIM Credit Repair LLC, we provide professional credit coaching and strategic dispute assistance to help you navigate this complex system. (For a step-by-step look at our full approach, including your rights under Minnesota law, see our guide on how credit repair works in Minnesota.) We work closely with you to:

- Conduct a comprehensive review of your credit reports from all three bureaus.

- Identify subtle reporting errors, compliance violations, and outdated information.

- Prepare and submit structured, compliant dispute packages on your behalf.

- Track responses and guide you on long-term credit-building strategies.

Please note: AIM Credit Repair LLC does not guarantee specific credit score increases, loan approvals, or the removal of accurate, verifiable negative information. Results vary based on individual credit profiles.

Take Control of Your Credit Today

Don't let reporting errors stand between you and your financial milestones. Contact Carlos Hawkins and the team at AIM Credit Repair LLC today to schedule your free, no-obligation credit consultation.

- Office Location: Hugo, Minnesota (Serving Minneapolis, St. Paul, Wyoming, and surrounding areas)

- Phone: (651) 333-7328

- Website: aimcreditfix.com

Frequently asked questions

How long does a credit dispute take in Minnesota?

Under federal law, credit bureaus must investigate and respond to your dispute within 30 days of receiving your letter. If they cannot verify the accuracy of the disputed item within that timeframe, they are legally required to update or delete it.

Can I dispute credit report errors on my own?

Yes. You have the absolute right to dispute any inaccurate information on your credit report for free directly with the credit bureaus. You do not need to hire a professional service to do this.

What is the Minnesota Credit Services Organization Act?

Minnesota Statutes Chapter 332G regulates credit repair companies operating in Minnesota. It grants residents the right to cancel any credit services agreement within 5 business days without penalty and prohibits companies from charging upfront fees before services are fully performed.